The eighth market scan conducted by the IAASB’s Disruptive Technology team explores the Internet of Things (IoT), focusing on Networks for Asset Monitoring and Data Generation. This technology enables real time tracking, management, and monitoring of business processes and assets. The article provides an overview of IoT, discusses its impact on the International Auditing and Assurance Standards Board (IAASB), and highlights the implications for audit and assurance.

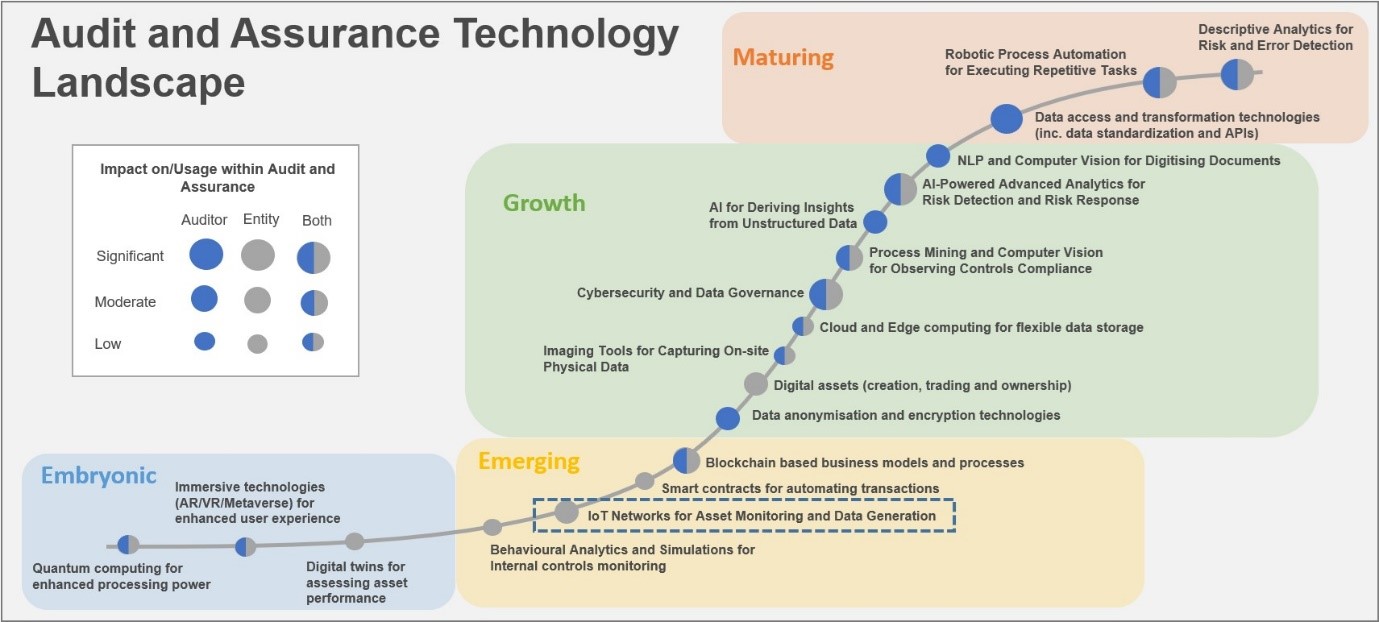

Initially, the article classifies IoT technology within the holistic context of an organization’s technology landscape, emphasizing its moderate impact and usage in the field of audit and assurance at the entity level.

This article highlights the importance of the IoT, provides a definition, and includes a link to a video for further explanation:

From an audit and assurance perspective, the article highlights two key implications of entity’s use of IoT devices and systems: Firstly, these technologies may be part of the entity’s internal control system, requiring consideration when assessing risks, including cybersecurity risks. Secondly, the data generated by IoT devices may be used in financial and non-financial reporting, such as sustainability disclosures, requiring auditors and assurance practitioners to consider the relevance, reliability, and the design of audit procedures.

The article also discusses recent developments in the IoT field, including the US National Institute of Standards and Technology’s selection of ‚Lightweight Cryptography‘ Algorithms for Small Device Protection and mentions start-up activities related to IoT systems and associated technologies.

In conclusion, the article addresses the potential impact of IoT on the IAASB. As the technology advances, it may introduce new risks and therefore have implications for the IAASB’s work, including future standard setting. Assurance providers will need to develop approaches to evaluate the relevance and reliability of information from IoT devices and consider how this information affects the design and performance of audit procedures. The article suggests that further standard-setting activities may be necessary to address specific implications of IoT technology in the field of audit and assurance.